(When to Use This: For clients who are highly technical, overly skeptical, or feel they “know more” about life insurance. Rather than arguing, educate.)

Intro:

You’ll meet clients who are engineers, analysts, or have read a few articles online and now think they’re experts. Early on, I used to try and prove I was smarter. But you don’t win by arguing. Let them win the ego game. You win by educating and staying composed.

When they ask:

- “Which policy is best?”

- “Why did the last guy say something different?”

- “Isn’t whole life better?”

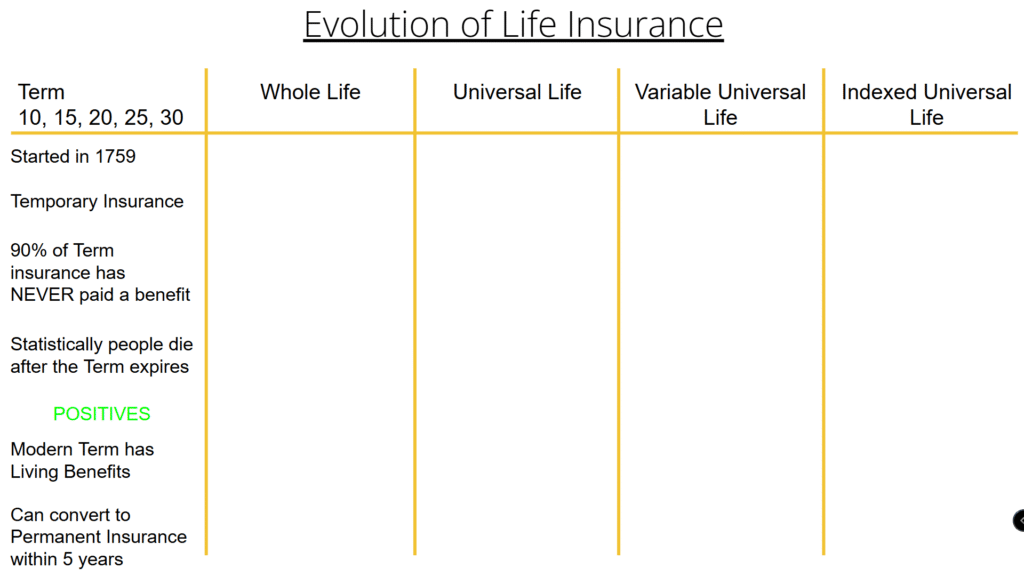

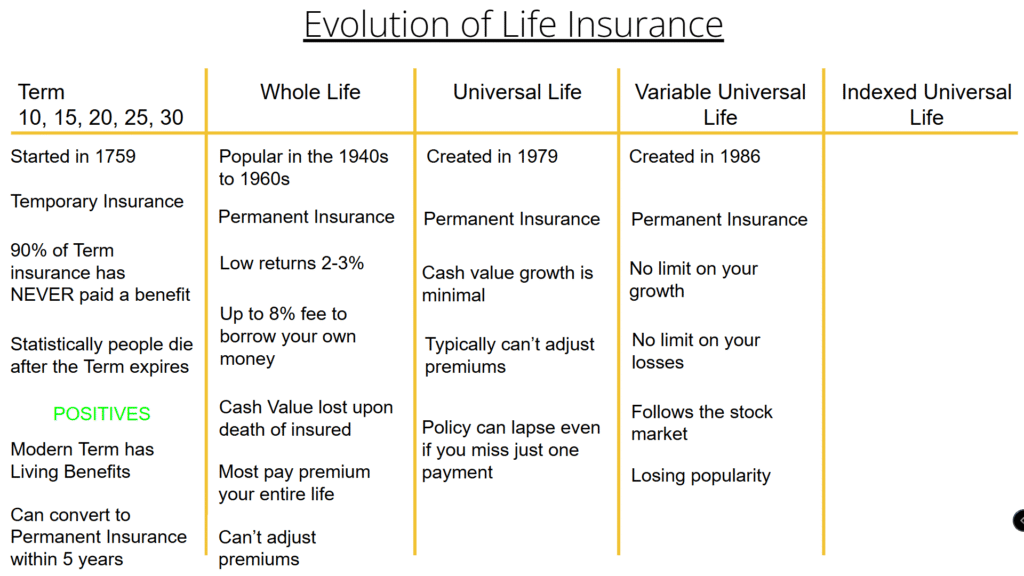

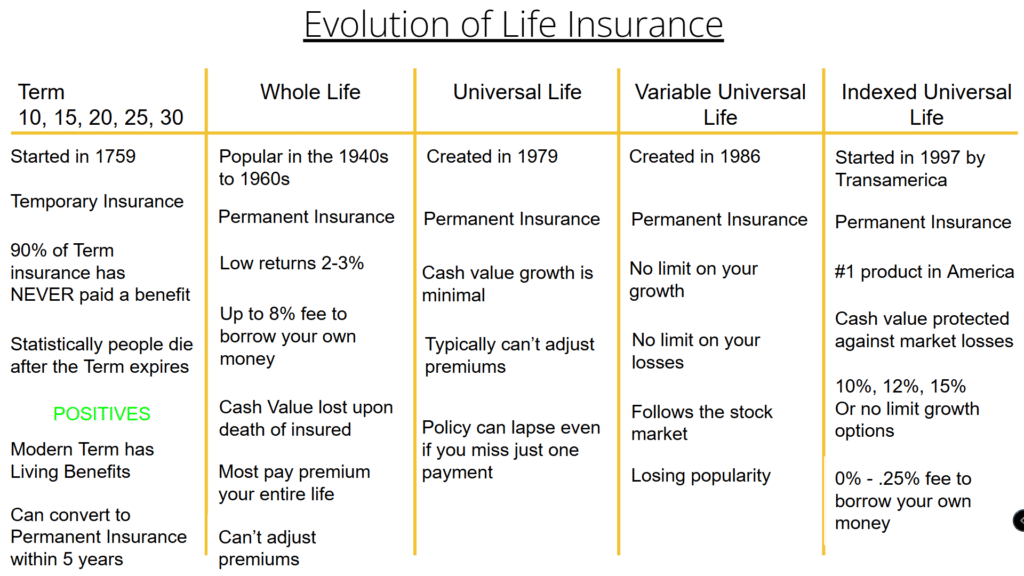

Instead of debating, I walk them through The Evolution of Life Insurance. It brings clarity. It shows facts. It builds trust.

1. Term Life Insurance

- Oldest & most basic form.

- Used primarily for protection.

- 99% of term policies never pay out because they expire or are canceled before death.

- Modern term policies include living benefits – like access to death benefit during critical, chronic, or terminal illness. That’s huge.

Use analogy: It’s like the foundation of a house. Without it, your financial “home” crumbles in a crisis. Term lays the groundwork, even if you can’t afford anything else right now.

✅ Key advantage: Can convert to permanent insurance (like an IUL) without re-qualifying for health. With the right company, you can do this any time during the life of the term, not just within the first few years.

Real Example:

I helped a client get a $1M term policy when she couldn’t afford to save or invest. Two years later, she was ready to start building wealth. We converted $350K of her term into an IUL – no medical exam needed. Now she has $650K in term and $350K in an IUL building cash value. Still fully protected.

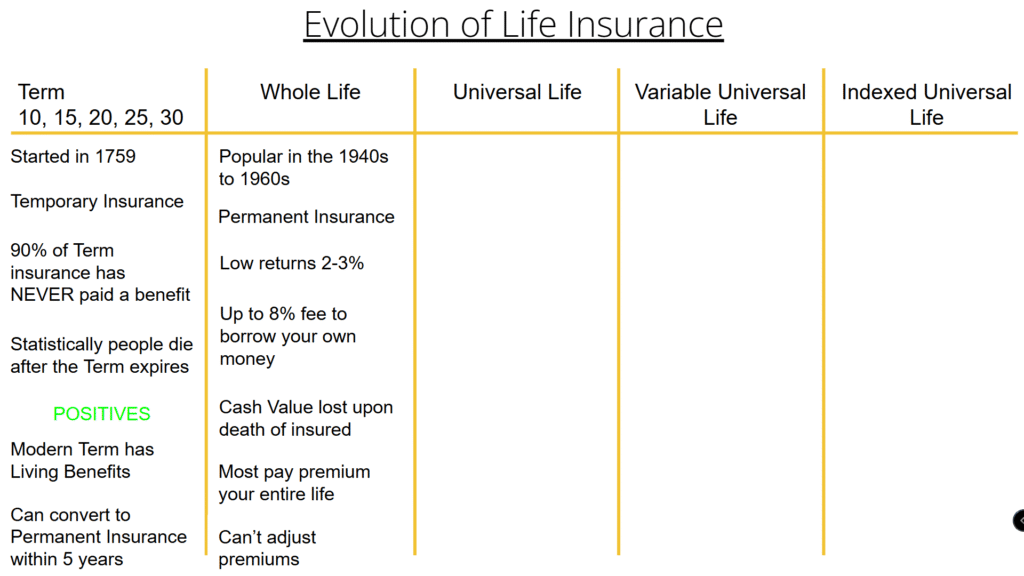

2. Whole Life Insurance

- Used to be the go-to solution.

- But the returns are limited, and borrowing your own money is expensive.

- Most whole life has a level death benefit, meaning your family only gets either the cash value or the death benefit—not both. That’s why we say:

🚫 “Level is the devil.”

It’s fixed. Fixed premium, fixed growth, fixed return.

If you’re someone who likes predictability and simplicity, it can still work. But there’s very little flexibility.

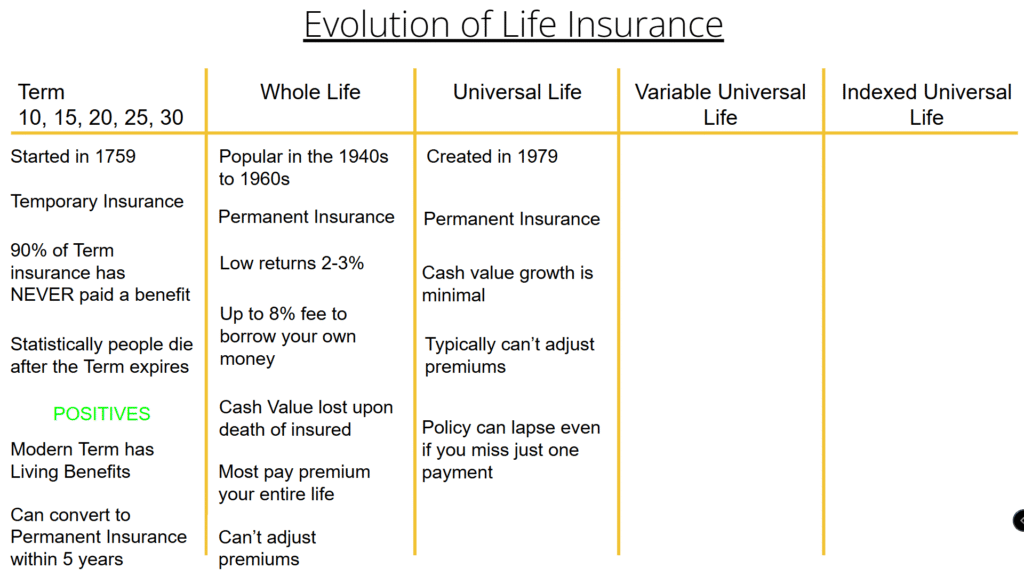

3. Universal Life (UL)

- Introduced in the 70s to create flexibility.

- Premiums could be adjusted.

- Cash value grew with high interest rates.

- But they were often underfunded, and many lapsed after missing just one payment.

4. Variable Universal Life (VUL)

- Introduced in the 80s during the boom of the 401(k).

- The goal? Put life insurance cash value into the stock market.

- Unlimited upside… and unlimited downside.

- Losing popularity now because clients don’t want negative returns or risk in their protection plan.

Some newer VULs have indexed features to mitigate risk, but they still carry more volatility.

5. Indexed Universal Life (IUL)

- Launched in 1997

- #1 product in America today for good reason.

- Tracks market indices like the S&P 500 — but with a floor of 0%, so you never lose money due to market downturns.

- Has high potential for returns (average over 8%, some policies hit 13% last year).

- More affordable to borrow from than whole life.

- Increasing death benefit options protect both your family and the cash value.

- Flexible, customizable, modern.

✅ Best of both worlds: Market-linked growth without market risk.

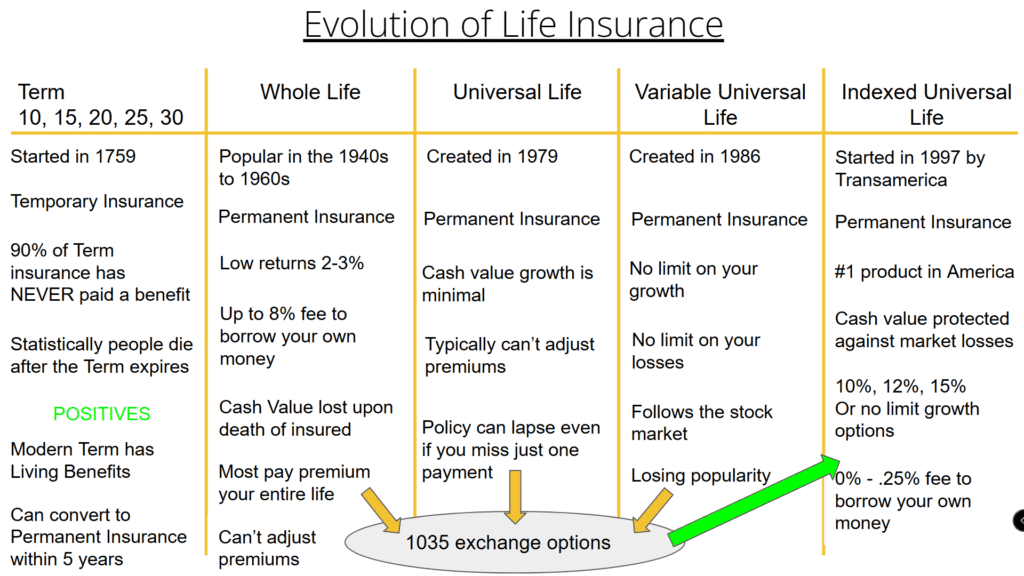

Common Question:

“What if something even better comes out?”

Great! We’ll do the same thing we’re doing for people now—move them from the old to the new. Through a 1035 exchange, we can transfer the cash value from a current policy into a better one, often with no tax consequences.

Final Thought:

You don’t need to argue about which life insurance type is “best.”

Educate. Show the history. Let the client decide.

And if they still don’t agree? That’s okay. Some people aren’t ready. But the numbers don’t lie—and they’ll remember the person who taught them when they’re finally ready to make the right move.

Leave a Reply